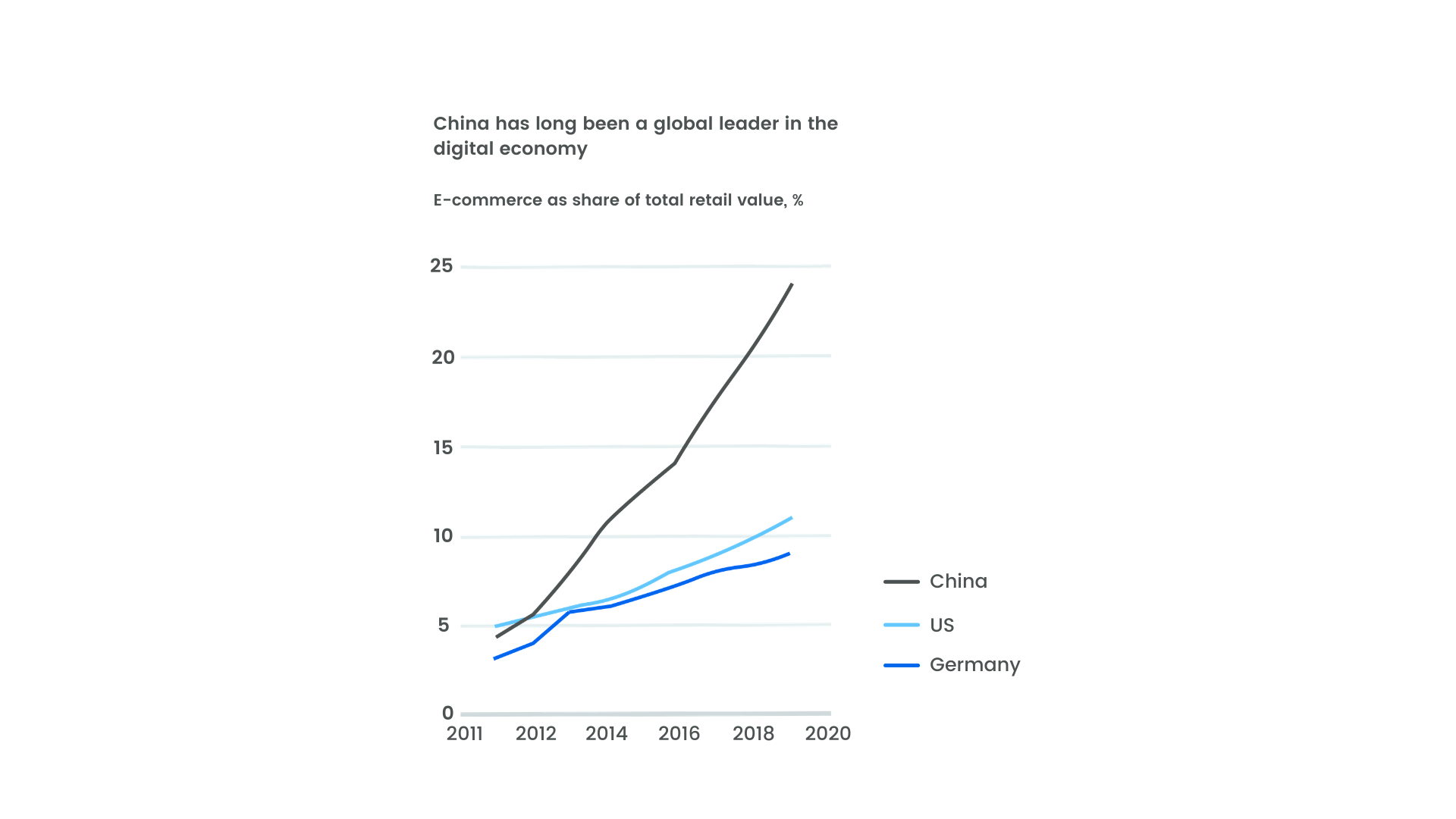

Much like what we’ve witnessed recently, the SARS outbreak in 2002 forced the Chinese and South Korean ecommerce markets to evolve, making them the most mature in the world. The closest Western equivalent is the UK. The retail customer model in China is more consumer-centric than the West, with a truly seamless, consistent omnichannel experience between online platforms as the norm.

Thanks to an already particularly digitized infrastructure, many of the client-consumer facing scenarios in the West have already been transformed into ecommerce transactions in China.

China’s digitalized CPG market is truly omnichannel

There are many examples that illustrate how the omnichannel shift will repeat in the US and Europe. One that is partially established is the penetration of the smartphone. Before the pandemic, mobile payment penetration in China was already triple that of the US. One effect of this has been social commerce being more common with digital word of mouth as an important driver of sales.

Emerging technologies will make efficient local fulfillment more common. JD, the Chinese ecomm giant, currently analyzes and determines the closest source for inventory, be it offline or a warehouse.

Virtual and augmented reality are also making inroads into the shopping experience in China, with high consumer enthusiasm and uptake.

The acceleration of the ecommerce ecosystem due to Covid

As mentioned, the pandemic has prompted the creation of new digital solutions for companies and consumers obliged to physically distance, driving growth of the “stay-at-home economy”.

China is more recovered from the recent COVID-19 epidemic than other countries, and it’s evident that a growth in online activity does not necessarily translate into growth in profits. Adapting to omnichannel has been expensive for CPG companies and transforming supply chains and internal organization to accelerate decision making and remove silos is not without costs, yet is essential to remain competitive.

Egrocery retail in post-pandemic China

One pre-existing trend that has accelerated in China is different from the West: an increase in the frequency of grocery purchases. In the US and Europe, frequency has declined while basket size has increased. Post-Covid, this may change as online purchasing becomes more habitual and the digital shelf optimized in the West.

Ultra-fast delivery has become essential in China and consequently, the need for small, local market delivery hubs has too, reminiscent of the urban click & collect points in France.

Supply chain management that traces the origins of food has become useful for younger consumers in particular in China, who are increasingly interested in the provenance and quality of their groceries, while yet not being as interested in organic foods as European shoppers.

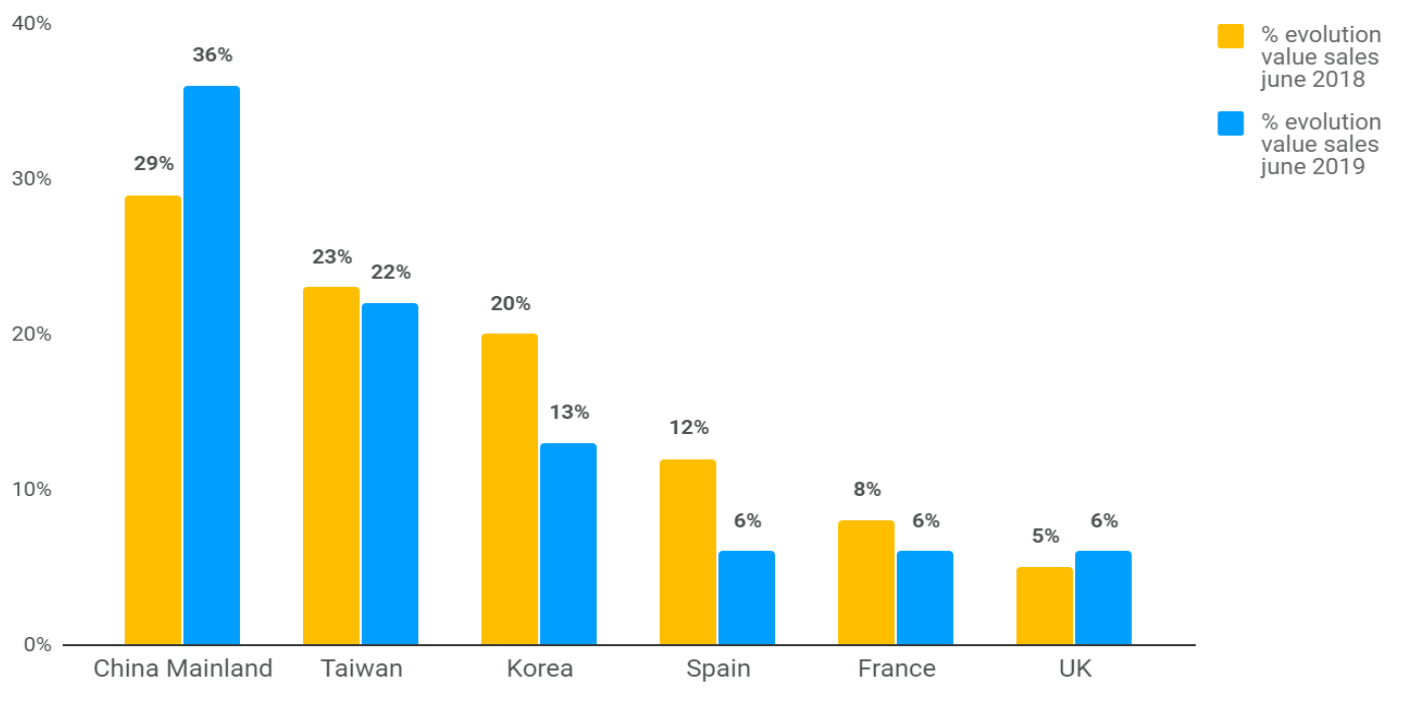

About 55 % of Chinese consumers are likely to continue buying more groceries online after the peak of the crisis

A particularity of China’s retail environment is that a significant portion of the market belongs to independent grocers. An opportunity has been seized upon by major players like Alibaba’s LST and JD’s XTL. They have created a digital B2B CPG space. By building on the success of their B2C ecommerce platforms, they are connecting independent stores directly with suppliers.

Digital B2B offers a one-stop service platform to small grocery retailers which is more convenient and efficient than interacting with sales representatives from multiple manufacturers and distributors. Inevitably, this will gradually make the whole CPG retail ecosystem more efficient.

DataImpact undertakes to ensure that the collection and processing of your data, carried out from the www.dataimpact.io site, comply with the Data Protection Act and the RGPD. This processing is necessary for the execution of our services and the internal functioning of our company. For any information on the protection of personal data, you can also consult the site of the Commission Informatique et Liberté www.cnil.fr.

Identity of the data owner:

Personal data are collected by : Société par actions simplifiée DataImpact whose registered office is at 39 Rue Lucien Sampaix, 75010 Paris, RCS PARIS 799 367 222 T: +33 (0)1 42 51 87 08

Purpose - use of your data:

DataImpact is likely to collect personal data about you for the purposes necessary for its activity, whether in terms of recruitment, responding to your requests for information, execution and monitoring of service contracts. Types of data collected: DataImpact only collects data that is strictly necessary for the purposes of its activity. The personal data collected can be the following:

-In the context of a request for information (name, first name, email, telephone, company name).

-As part of a recruitment process: (surname, first name, email, telephone, company name), information on the curriculum vitae (marital status, surname, first name, date and place of birth, nationality, professional background, academic background, hobbies)

-If necessary, connection data including your IP address may be collected for purely statistical purposes.

Origin of the data:

The personal data collected by DataImpact are those directly given by the person concerned when using the contact form or surfing on the site www.dataimpact.io.

Intended transfers of personal data to a non-EU Member State:

To date, DataImpact does not transfer, nor envisage any transfer of your personal data to a non-European Union member state.

Retention period of the categories of data processed:

Connection data are kept at the latest within one year after connection to the www.dataimpact.io website. Data relating to applicants for a post are kept at the latest five years after the last contact, with a view to possible recruitment.

Data of prospects are kept no later than three years after the last contact.

Customer data are kept for the duration of the service contract.

Protection of your data:

DataImpact ensures that its employees and service providers, subcontractors or hosts, also respect the absolute confidentiality of the information provided to them.

We maintain in-house electronic and organizational security measures in relation to the collection, storage, and communication of data.

Your rights under the Data Protection Act:

DataImpact takes all appropriate measures in order to facilitate the exercise of the rights of its clients regarding their personal data (right of access, rectification, deletion, limitation of processing, portability, to define the fate of its data after death).

The information provided in connection with the exercise of these rights is provided in writing or electronically. On request, the information may be provided orally. All requests should be sent by post to 739 Rue Lucien Sampaix, 75010 Paris or to [email protected].

In accordance with the regulations in force, your request must be signed and accompanied by a photocopy of an identity document bearing your signature and specify the address to which the reply should be sent. A reply will then be sent to you as soon as possible and in any event within one month of receipt of the request.

Flows out of your data after your death:

The new article 40-1 of the French Data Protection Act allows individuals to give instructions regarding the storage, deletion and communication of their data after their death.

You can read the procedure relating to these directives by following the following link: “https://www.cnil.fr/fr/ce-que-change-la-loi-pour-une-republique-numerique-pour-la-protection-des-donneespersonnelles#mortnumerique”.

Cookies:

You are informed that, during your visits to the www.dataimpact.io website, a cookie may, if necessary, be automatically installed on your browser software. A cookie is a small file stored on your computer. As such, it is a block of data that does not allow users to be identified but is used to record information relating to their browsing on the site. Cookies are used, on the one hand, to facilitate your navigation on the site and, on the other hand, for statistical purposes. In order to better know the frequentation of the site, we (mainly) measure the number of pages viewed, visitors, visits, as well as the activity of visitors on our site and their frequency of return.

The parameters of the browser software make it possible to inform about the presence of cookies and possibly to refuse them in the manner described at the following address “http://www.cnil.fr/vos-libertes/vos-traces/les-cookies/”.

You have the right to access, withdraw and modify personal data communicated through cookies under the conditions indicated above.

Terms of Service

Article 6 III of the Law of 22 June 2004

Société par action simplifiée DataImpact 39 Rue Lucien Sampaix, 75010 Paris T: +33 (0)1 42 51 87 08 M: [email protected] RCS PARIS 799 367 222

The information contained and consultable on this site is provided for information purposes by DataImpact. They can be modified at any time without notice. Under no circumstances does it constitute advice or a service of any kind whatsoever. You assume full responsibility for the use of this site or the information it contains.

DataImpact cannot be held responsible for damages related to the consultation or use of the website by the user. Hypertext links may refer to third party sites over which DataImpact has no control.

DataImpact declines all responsibility for the content of these sites. The use of this service is reserved for strictly personal use. Any reproduction or representation, of all or part of the information, brochures or logos contained on the site, on any medium whatsoever, is prohibited. Failure to comply with this prohibition constitutes an infringement that may result in civil and criminal liability of the counterfeiter.